Private Equity Due Diligence: What You Need To Know

Every target company looks flawless in a polished investment memorandum—and that’s where private equity due diligence comes in. But take note: Thorough due diligence is about more than just uncovering hidden liabilities before you reach the closing table.

A great deal team doesn’t just look for red flags. These teams also surface the operational improvements, pricing power, and margin expansion opportunities that validate the core investment thesis and shape the 100-day plan for limited partners. These findings ultimately dictate whether a deal closes, at what price, and under what terms.

This article provides a practical look at what private equity due diligence involves, the essential workstreams to prioritize, and the critical red flags to spot. We'll also explore how private equity deal teams scale these efforts using AI-powered tools like Hebbia to automate complex diligence.

What Is Private Equity Due Diligence?

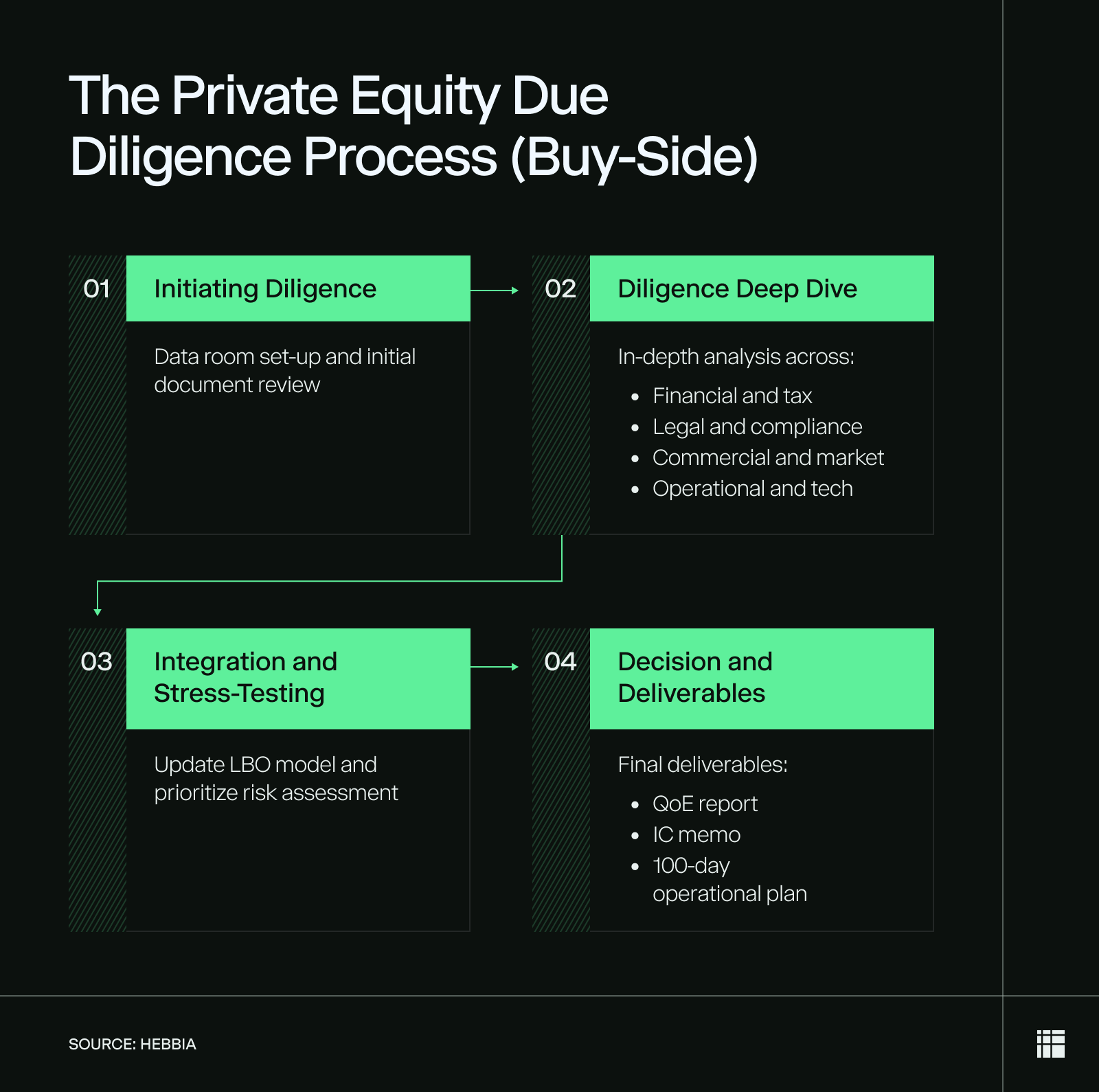

Private equity (PE) due diligence is the deep-dive review that a buy-side private equity firm conducts on a target company before investing. It’s where the deal team moves past the polished pitch deck, Confidential Information Memorandum (CIM), or management presentation to see what the business actually looks like under the hood.

Beyond catching red flags, diligence validates the private equity firm’s investment thesis and maps out the specific pricing, margin, and operational levers that will drive returns post-close.

These findings directly impact the deal's structure and pricing. This data is then packaged into the final deliverables presented to the investment committee and LPs.

Typical outputs of a buy-side diligence process include:

- Valuation model (LBO model): A leveraged buyout model stress-tested with real data to ensure the deal hits target returns.

- Quality of Earnings (QoE) report: An independent financial analysis that verifies true profitability and sets the net working capital peg, which is the baseline for liquidity at closing.

- Representations and warranties: The legal statements and indemnification terms in the final purchase agreement, informed by the diligence findings and typically backed by representations and warranties insurance (RWI).

- Risk matrix: A list of legal and operational vulnerabilities used to negotiate protective terms or purchase price adjustments before closing.

- Investment Committee (IC) memo: The final, data-backed document used to pitch the deal to fund partners for capital approval.

- 100-day plan: The post-acquisition operational blueprint detailing the exact changes needed to grow the business immediately after closing.

Core Objectives of the Diligence Process

Every fund has its own investment style, but effective due diligence always anchors on three core objectives. Hitting these targets ensures you base your investment on hard facts rather than management assumptions:

- Confirming purchase price/valuation: You need to verify that the target's actual financial health justifies the multiple offered in the Letter of Intent (LOI). This protects the fund from overpaying based on unsustainable revenue or inflated numbers.

- Identifying post-closing value creation levers: Diligence provides the baseline for your future returns by uncovering real operational opportunities. It helps you identify immediate pricing power, cost-savings, and margin-expansion levers to build directly into your 100-day plan.

- Uncovering deal-breakers or risks: This involves hunting for hidden liabilities, like pending lawsuits or critical customer concentration, that could destroy the investment thesis. If a risk isn't a deal-killer, it gives you the exact leverage needed to renegotiate the price or draft protective legal terms.

The Four Essential PE Due Diligence Workflows

Executing due diligence requires running multiple specialized analytical streams simultaneously. Because these workflows overlap, continuous communication between teams is the only way to avoid missing critical details.

Managing these workflows effectively prevents deal teams from getting blindsided by hidden costs or structural issues.

Focus on these four essential areas to properly pressure-test every angle of your investment thesis.

1. Financial and Tax Due Diligence

Financial diligence focuses on verifying a target company's real earnings. Instead of relying on standard audits, deal teams hire a Big Four or specialist firm to build a QoE report. This report analyzes revenue quality and strips out management's one-time add-backs to find the true, sustainable adjusted EBITDA.

At the same time, tax advisors review historical returns to flag deferred liabilities, transfer pricing risks, and deal structuring opportunities. The financial team also looks at seasonal cash flows to calculate a normalized working capital peg.

Because this peg dictates how much cash must be left in the business on day one, it becomes a major negotiation point that directly impacts the final purchase price.

Financial due diligence checklist:

- Commission an independent QoE report to assess EBITDA sustainability, normalize add-backs, and identify revenue quality risks not visible in audited financials.

- Calculate and negotiate the normalized working capital peg, accounting for seasonality. This directly affects post-close price adjustments.

- Review historical tax returns with a qualified tax advisor to identify deferred liabilities, aggressive positions, and transaction structuring implications

2. Legal Due Diligence

Legal diligence maps out a target company's liabilities and verifies that the seller has the legal right to transfer the business.

The legal team focuses heavily on analyzing material contracts for restrictive covenants, exclusivity clauses, and change-of-control provisions. Identifying these clauses upfront discourages a key customer or vendor from unexpectedly canceling their agreement, demanding a payout, or blocking the transaction entirely post-close.

This workflow also evaluates the target's corporate structure, pending lawsuits, and regulatory compliance. At the same time, advisors review the capitalization table to verify that all past equity ownership is completely clean.

For tech or branded consumer businesses, the team conducts extensive intellectual property (IP) reviews to ensure the target fully owns its core assets. This involves auditing patents, trademarks, employee IP assignments, and open-source software compliance.

Legal due diligence checklist:

- Review all material customer and vendor contracts for change-of-control clauses and restrictive covenants.

- Validate the capitalization table and trace all historical equity issuances.

- Confirm ownership and assignment of all material IP, including employee/contractor IP agreements and any open-source licensing obligations.

- Evaluate pending or threatened litigation and regulatory compliance history.

3. Commercial and Market Due Diligence

Commercial diligence tests whether the target company can actually achieve its projected growth. Deal teams pressure-test management's market claims rather than taking their internal forecasts at face value.

To do this, funds often hire third-party commercial advisors to build an independent market model. This model analyzes industry headwinds and tailwinds to verify or challenge management's assumptions about their Total Addressable Market (TAM) and future growth runway.

The team also runs blind voice-of-customer (VoC) interviews with current and former clients to test the value proposition anonymously. Comparing these insights against customer concentration and churn data shows whether top-line revenue is secure or fragile.

Commercial and market due diligence checklist:

- Map out customer concentration and calculate cohort-level churn.

- Conduct blind voice-of-customer (VoC) interviews to validate the value proposition.

- Assess total addressable market (TAM) growth rate vs. the target's growth using an independent market model.

4. Operational and Technology Due Diligence

Operational and technical diligence assesses whether the company's infrastructure, team, and systems can support your three-to-five-year growth plan. Deal teams look beyond current performance to find where the business will break under higher volumes.

This means testing the supply chain for capacity limits and auditing software applications. Crucially, the team must confirm that core IT systems can scale smoothly without requiring an immediate, expensive overhaul.

This stream also catches deferred capital expenditure (CapEx) and organizational risks. Sellers often inflate margins by delaying tech or equipment upgrades right before a sale. Spotting this early lets you build those costs directly into your valuation model. At the same time, the review flags key-man dependencies to ensure middle management can support the growth.

Operational due diligence checklist:

- Audit historical CapEx to ensure the business hasn't been starved of investment.

- Identify key-man dependencies and evaluate the depth of the middle-management layer.

- Assess the scalability of the current IT infrastructure and identify technical debt.

Common Red Flags to Watch For

Diligence requires actively hunting and managing risks that could break your investment thesis or force a price renegotiation. The most dangerous red flags rarely appear in the initial pitch deck or on standard financial statements.

Instead, they are buried deep within granular data room files, requiring the deal team to spot systemic issues before committing capital.

When auditing a data room, deal teams should prioritize watching for these four critical warning signs, starting with hidden vulnerabilities in the revenue base:

Customer Concentration and Churn

High customer concentration is a classic private equity pitfall that can instantly break a deal's economics. If a target company relies on a few massive clients for a large percentage of its revenue, losing just one account post-close can destroy the fund's projected returns.

Deal teams need to look past aggregate numbers to analyze the specific contract terms, renewal dates, and termination clauses for these top accounts.

A more dangerous variation occurs when a few large, expanding accounts mask a high customer churn rate. Top-line revenue might look stable or growing, but cohort-level analysis often reveals that the business is rapidly losing smaller customers. This pattern indicates poor product-market fit and leaves the company heavily exposed if its primary clients pull back.

Aggressive Pro-Forma Add-Backs

Sellers often use aggressive pro-forma add-backs to inflate EBITDA, forcing deal teams to separate genuine adjustments from management optimism. The first common trap involves structural costs masked as non-recurring expenses, like a "one-time" IT consulting fee that actually appears in the general ledger every year.

The second issue involves legitimate add-backs that are unsubstantiated or overvalued. For instance, management might claim a departing founder’s $600,000 salary will be replaced by a $200,000 hire. The deal team must independently test whether that lower rate can actually attract the right executive talent.

The most aggressive management assumptions usually live in a separate category: pro-forma synergies and future run-rate cost savings. Sellers frequently project these adjustments by assuming immediate vendor discounts or operational efficiencies post-close without doing any real integration planning.

Because these forward-looking numbers directly alter the purchase price, the financial and operational teams must independently validate them before baking them into the LBO model.

Key-Man Risk and Founder Dependency

Investors frequently run into "hero culture" when evaluating middle-market or founder-led businesses.

When a company relies entirely on the personal relationships, charisma, or tribal knowledge of the founder or a single star salesperson, it lacks true institutional value. Without repeatable operational systems and an empowered team, the business functions more like an individual's high-paying job than a scalable enterprise.

This dependency threatens the entire investment thesis the moment the founder cashes out or steps away from daily operations. If customer loyalty belongs to a single person rather than the brand or product, revenue can quickly evaporate post-close.

Diligence teams must evaluate how easily these critical relationships and operational processes can be transitioned to new leadership without disrupting the business.

Deferred Capital Expenditure (CapEx)

Sellers frequently freeze spending on equipment, facilities, or software updates 12 to 18 months before launching a sale process. This tactic artificially inflates free cash flow by cutting back on maintenance CapEx—the baseline capital needed just to keep the business running—rather than growth CapEx meant for expansion.

When a company underinvests in its core assets, its reported cash flow looks deceptively strong, masking the true operational costs of the business.

Failing to spot this dynamic leaves the buyer with a massive Day 1 tech debt or infrastructure bill that can instantly tank the LBO model's returns.

To avoid this, diligence teams estimate a true maintenance CapEx baseline by analyzing asset age, historical replacement cycles, and industry peer benchmarks. They then use this normalized figure to rebuild the free cash flow model, ensuring the fund doesn't overpay for starved infrastructure.

How Modern PE Deal Teams Scale Due Diligence With AI

Deals rarely fail because teams don't know what to look for—they simply run out of time to find critical risks before exclusivity expires. Advanced AI finance analysis platforms, like Hebbia, have become table stakes for top-tier funds by completely eliminating the traditional trade-off between thoroughness and speed.

Instead of relying on random sampling, investors can now audit 100% of the data room. This protects institutional-grade accuracy without sacrificing deal speed. Specifically, these platforms redefine the diligence process across four key areas:

- Find what "Ctrl + F" misses: When a data room holds hundreds of vendor or customer contracts, even a well-designed legal review misses things. This happens because full human coverage is physically impossible within a tight three-week window, not because reviewers lack expertise. AI for private equity handles the volume by querying the entire document stack simultaneously, ensuring no structural risk goes unreviewed.

- Audit 100% of the data room: Tight exclusivity windows frequently force even experienced deal teams to sample only a fraction of contracts—typically the top 10 to 20 by revenue—leaving the long tail completely unexamined. AI eliminates these dangerous blind spots by instantly indexing and analyzing every single lease, contract, and compliance file in the virtual data room (VDR).

- Connect the dots across different documents: AI platforms instantly cross-reference isolated data points across entirely separate workstreams. For example, the software can link an obscure footnote in a financial QoE report to a specific indemnification clause buried deep in a legal agreement, surfacing hidden liabilities a human reviewer might only find by pure luck.

- Eliminate the speed vs. accuracy trade-off: Traditionally, conducting a truly exhaustive review meant moving slowly, which risked losing exclusivity or letting a deal go cold. AI enables teams to maintain absolute accuracy and institutional depth without sacrificing the rapid execution required to stay competitive.

Drive Deeper Diligence With Hebbia

Private equity due diligence is a foundational pillar of deal execution, but manual document review introduces massive risk at every step. As deal timelines compress and virtual data rooms expand into thousands of files, the traditional approach of having junior deal team members dig through endless PDFs simply doesn't scale.

Hebbia automates the entire document analysis process by instantly pulling customer concentration data, change-of-control clauses, and hidden financial liabilities from across your VDR in minutes instead of weeks. Every insight is cited directly back to the source text, giving you the ironclad audit trail your investment committee demands.

From deep dives to tight exclusivity windows, Hebbia eliminates manual search fatigue and prevents missed red flags that cost millions.

Request a demo today to see how Hebbia can streamline your due diligence workflow.