Credit Risk Modeling: Types, Techniques, and AI-Driven Transformation

In credit, where the upside is capped and avoiding losses is paramount, missing even one small detail in a contract can lead to catastrophic results. While 46% of financial professionals report being overwhelmed by the sheer volume of documents they must parse, the primary danger isn't the administrative burden—it’s the inherent risk of human error during manual review.

Credit risk modeling serves as the primary defense against these outcomes by identifying, quantifying, and mitigating core financial risks. Effective modeling goes beyond basic financial metrics to incorporate deep analysis of unstructured data in financial and legal documentation and in virtual data rooms (VDRs).

This guide explores how sophisticated credit modeling can transform a manual administrative burden into a competitive advantage, allowing teams to protect against downside risks.

What Is Credit Risk?

Credit risk is the likelihood that a borrower will default on a loan or fail to meet contractual obligations, resulting in significant financial loss for the lender or investor. For credit investors, whether they’re evaluating private loans or publicly traded bonds, this risk sits at the center of every investment decision.

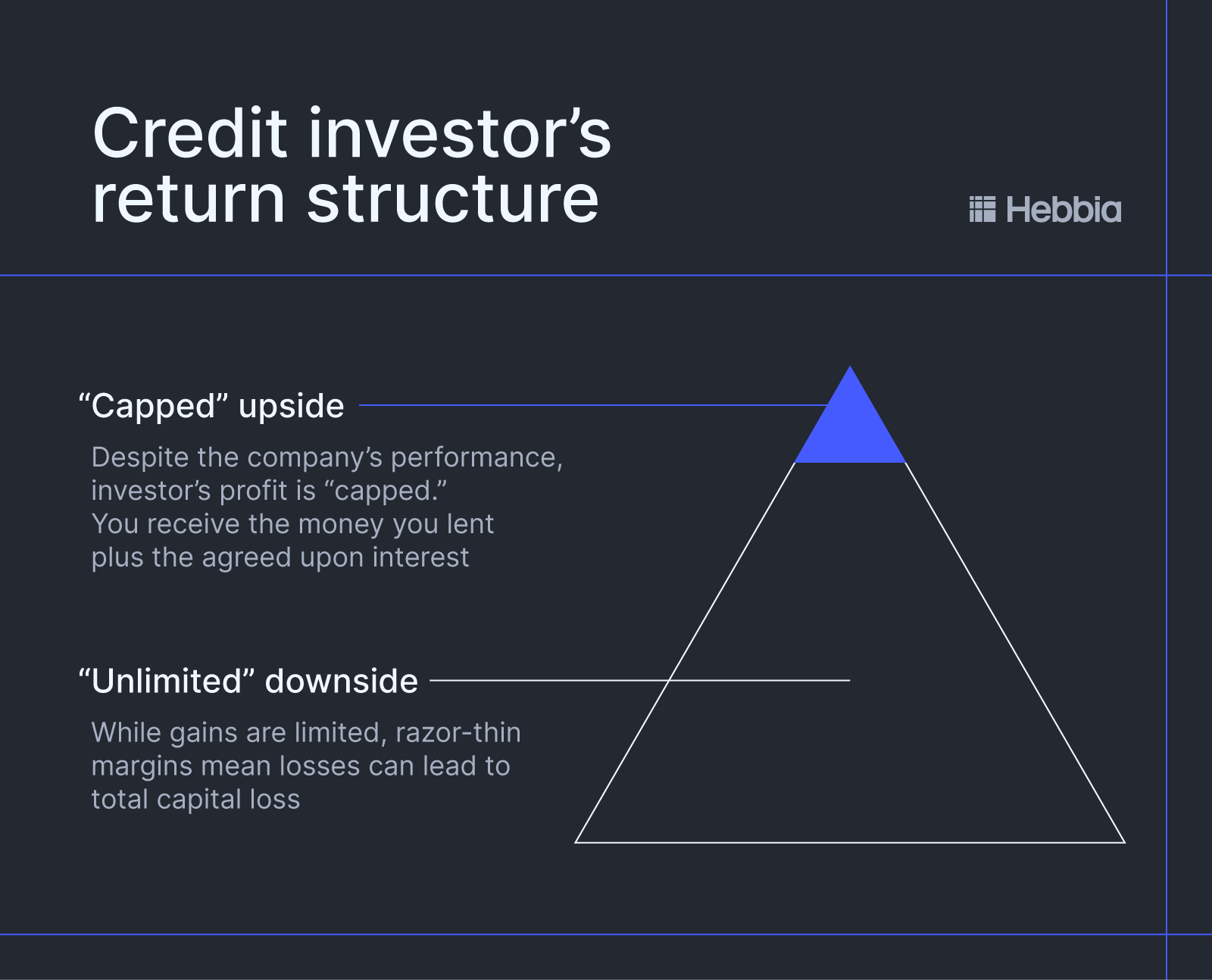

Unlike equity investors who can capture unlimited upside, credit investors face a fundamentally different return structure:

- Capped upside: Returns are limited to principal plus interest

- Unlimited downside: Potential for total capital loss

- Outcome: Avoiding losses matters more than identifying winners

This asymmetry shapes everything. The best-case scenario is receiving payment on time. The worst case is total capital loss. Credit professionals get penalized for risks they failed to anticipate.

For credit investors managing portfolios across private loans and liquid bonds, continuously monitoring performance versus expectations, ensuring compliance with covenants, and identifying early warning signals buried in quarterly filings is essential. In credit, missing a risk means missing everything. The margin for error is razor-thin.

Types of Credit Risk

Credit risk takes multiple forms, each requiring distinct monitoring and mitigation strategies. Effective models must evaluate both a borrower’s financial strength and the legal terms of the deal. Consequently, credit risk modeling must account for the measurable probability of default while also verifying the specific contractual protections that safeguard a lender's position.

- Default risk: The most direct form of credit risk—the possibility that a borrower fails to make timely principal or interest payments, resulting in immediate financial loss and potential recovery proceedings.

- Downgrade or spread risk: The potential for a borrower's creditworthiness to deteriorate over time, leading to rating downgrades that widen credit spreads and reduce the market value of debt holdings even before any payment is missed.

- Concentration risk: Overexposure to a single borrower, industry, or geographic region that creates correlated losses when adverse events impact multiple positions simultaneously, amplifying portfolio volatility.

- Sovereign or country risk: The possibility that political instability, regulatory shifts, currency controls, sanctions, or broader macroeconomic deterioration in a country impair a borrower’s ability to repay, even when the borrower’s standalone fundamentals appear sound.

- Counterpart risk: The risk that the other party in a financial transaction—such as a derivative, hedge, financing arrangement, or trade settlement—fails to meet its contractual obligations, creating losses tied not just to credit quality but also to timing, exposure, and market conditions.

- Documentation and covenant risk: The danger that weak loan documentation, permissive covenant language, carve-outs, baskets, or structural loopholes limit lender protections, making it harder to detect problems early, enforce remedies, or preserve value in a downside scenario.

What Is Credit Risk Modeling?

Credit risk modeling is the process of quantifying the likelihood of default and estimating potential financial losses to inform investment and lending decisions. These models translate complex borrower information into measurable risk metrics that guide portfolio construction, pricing, and ongoing monitoring.

Effective credit risk modeling requires both statistical rigor and expert judgment:

Quantitative data | Qualitative data |

|---|---|

- Historical default rates and recovery data - Financial ratios and leverage metrics - Macroeconomic indicators and correlations - Statistical models and probability distributions | - Dense credit agreements and covenant structures - Management commentary in earnings transcripts - Language changes in quarterly filings - Industry dynamics and competitive positioning |

This isn't a static exercise. Analysts must continuously recalibrate their views based on:

- New financial data and performance trends

- Market shifts and spread movements

- Emerging risks in covenant compliance

- Changes in macroeconomic conditions

Models calibrated to last year's market regime can become obsolete overnight. The analysts who outperform identify inflection points early, before covenants are breached, spreads widen, and markets reprice risk.

Key Components of Credit Risk Modeling

Credit risk analysis models rely on probability of default (PD), loss given default (LGD), exposure at default (EAD), and credit valuation adjustment (CVA). These four metrics work together to quantify potential losses and inform risk-adjusted pricing decisions:

- Probability of default (PD): The likelihood that a borrower will default within a specific time period, typically expressed as a percentage over one year. PD is derived from historical default rates, financial ratios, credit ratings, and borrower-specific risk factors.

- Loss given default (LGD): The anticipated percentage of total exposure that will be lost if a default occurs, accounting for expected recoveries from collateral, guarantees, or bankruptcy proceedings. LGD varies significantly based on seniority, security, and the quality of underlying assets.

- Exposure at default (EAD): The total amount a lender is exposed to at the moment of default, including outstanding principal, accrued interest, and any undrawn commitments that may be drawn down before or during distress. For revolving credit facilities, EAD can be substantially higher.

- Credit valuation adjustment (CVA): The adjustment to a bond's or loan's fair value to account for the market's pricing of default risk, reflecting the expected loss from potential counterparty default. CVA translates credit risk metrics into mark-to-market impacts, which is particularly important for liquid credit portfolios where unrealized losses matter as much as actual defaults.

Main Model Types

Credit risk modeling has evolved from simple statistical approaches to sophisticated machine learning frameworks, each with distinct strengths for different credit applications and portfolio contexts:

Structural Models

Structural models treat a firm's equity as a call option on its total assets, with default occurring when asset values fall below liabilities. Rooted in the Merton Model and the Black-Scholes framework, these models transform observable equity market signals—such as stock prices, volatility, and debt structure—into forward-looking default probabilities.

They depend on specific market data and are best suited for particular credit applications:

Data required | Primary applications |

|---|---|

Market value of equity | Estimating the probability of default (PD) for publicly traded companies |

Equity volatility | Real-time credit risk monitoring using market signals |

Risk-free interest rates | Portfolio risk management for liquid credit |

Face value and maturity of liabilities | Credit spread decomposition and relative value analysis |

Structural models excel when equity market data is readily available and reliable, making them particularly valuable for liquid credit investors monitoring public bond issuers. They provide forward-looking, market-based default probabilities that update continuously as equity prices and volatility shift.

However, they only work for publicly traded companies and rely on simplified assumptions about capital structure and volatility that don't always reflect reality.

Reduced-Form Models

Reduced-form models, also known as hazard rate or intensity-based models, focus on predicting when a default might occur rather than explaining why it happens. Default is treated as a random event that can occur at any moment, with the probability changing over time based on market conditions and economic factors.

These models estimate a hazard rate—the likelihood of default at any given point—that fluctuates with macroeconomic trends, market sentiment, and firm-specific characteristics. Unlike structural models that derive default risk from asset values, reduced-form models calibrate directly to observable market prices like credit spreads:

Data required | Primary applications |

|---|---|

Macroeconomic indicators (GDP, interest rates, unemployment) | Pricing credit derivatives and CDS contracts |

Market data (credit spreads, bond prices) | Valuing defaultable bonds across credit quality |

Historical default rates by sector and rating | Portfolio risk modeling for entities without traded equity |

Recovery rate assumptions | Municipal credit and private company credit risk assessment |

Reduced-form models are particularly valuable for pricing credit derivatives and modeling risk for entities without observable asset values, such as municipal governments, private companies, or structured credits. They incorporate market-implied information and adapt flexibly to changing conditions.

These credit risk assessment models don't examine the fundamental economic reasons behind default, relying instead on statistical patterns and market pricing. Their accuracy depends on high-quality calibration data and the assumption that historical hazard rates remain stable over time.

Transition and Portfolio Models

Transition and portfolio models estimate how obligors migrate across rating buckets and how defaults cluster under stress. These frameworks are useful when the real question is not just “Will this borrower default?” but “How could a portfolio behave if spreads widen, recoveries fall, and defaults become correlated?” They are especially relevant for portfolio construction, regulatory stress testing, capital planning, and concentration management.

These models typically rely on a mix of historical credit performance, portfolio exposure data, and macroeconomic assumptions:

Data required | Primary applications |

|---|---|

Historical default rates by sector and rating | Estimating default and migration risk across a portfolio |

Rating transition matrices | Modeling changes in borrower credit quality over time |

Correlation and recovery assumptions | Projecting clustered defaults and loss severity under stress |

Macroeconomic indicators (GDP, interest rates, unemployment) | Running scenario analysis and regulatory stress tests |

Exposure data by borrower, industry, or geography | Measuring concentration risk and portfolio vulnerability |

Their strength is portfolio-level realism; their weakness is that outputs are highly sensitive to correlation, scenario, and calibration choices.

Credit Scorecards

Credit scorecards are statistical models that rank individual or corporate borrowers by creditworthiness, assigning numerical scores that quantify the probability of repayment.

These models employ a lookup table approach, where specific borrower characteristics—such as income level, payment history, and debt ratios—are translated into points, and the total score corresponds to an estimated risk level.

Scorecards are designed for speed and consistency, making them ideal for high-volume lending decisions where manual underwriting would be impractical:

Data required | Primary applications |

|---|---|

Application data: Income, employment status, debt-to-income ratios | Automating high-volume loan approvals (consumer credit, small business lending) |

Bureau data: Payment history, length of credit history, outstanding debt | Setting interest rates and credit limits based on risk tiers |

Behavioral data: Transactional history, spending patterns, account utilization | Prioritizing delinquent accounts for collection efforts |

Scorecards standardize credit decisions across thousands or millions of borrowers, reducing human bias and processing time in consumer lending and increasingly in small business credit assessment.

However, credit scorecards are backward-looking, relying on historical patterns that may miss emerging risks or changing borrower circumstances. Scorecards also struggle with borrowers who lack extensive credit histories, and their points-based approach can oversimplify complex situations that require judgment beyond what numerical scores capture.

Methods and Techniques

Credit risk techniques now split into three layers: interpretable statistical models for baseline estimation, simulation frameworks for scenario and portfolio analysis, and AI systems that read the unstructured context traditional models ignore. The strongest credit stacks use all three.

Statistical Techniques

Statistical techniques form the foundation of credit risk modeling, providing transparent and interpretable approaches to predicting default probability. These models use historical financial data to establish baseline credit assessments for deal sourcing and portfolio monitoring. They're explainable, showing exactly which variables drive risk predictions, which is critical for investment committee approvals and regulatory reviews.

The most widely used approaches include:

- Logistic regression: Calculates default probability based on leverage ratios, interest coverage, and liquidity metrics. The model quantifies the marginal impact of each risk factor, making it straightforward to explain which variables contribute most to credit risk.

- Decision trees: Segments borrowers into risk categories based on specific financial thresholds (e.g., debt-to-EBITDA above 6x, interest coverage below 2x). These are particularly useful for creating clear, rule-based underwriting criteria that credit teams can apply consistently.

- Altman Z-score: Combines five financial ratios—working capital to assets, retained earnings to assets, EBIT to assets, market value of equity to liabilities, and sales to assets—to predict bankruptcy probability within two years. It remains widely used as a quick health check for corporate borrowers.

- Gradient boosting and random forests: Useful for rank-ordering risk and surfacing complex interactions across financial, behavioral, and operational variables. Because these models can be harder to interpret, they work best when paired with feature attribution, challenger models, and human review.

These techniques are great for consistent, repeatable credit assessments across established borrowers. However, they rely on historical financial data and struggle to capture non-linear relationships or complex interactions that advanced AI models can detect.

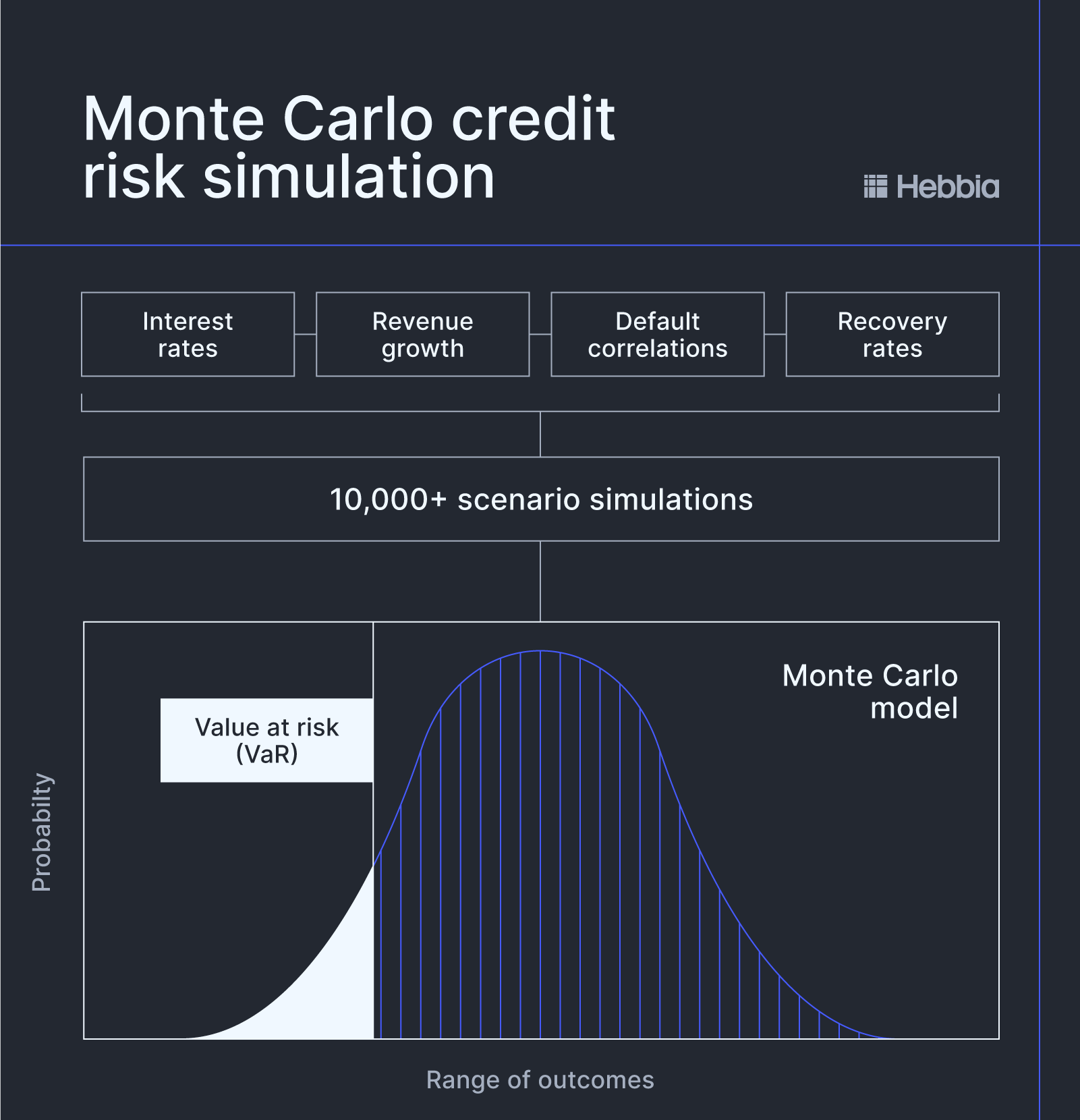

Monte Carlo Simulations

Monte Carlo simulations model credit risk by running thousands of possible scenarios to understand how portfolios might perform under different conditions. Rather than relying on single-point estimates, these simulations generate probability distributions of potential outcomes, which is particularly useful for assessing credit migration (rating downgrades) and calculating Value at Risk (VaR) for complex debt portfolios over long horizons.

Here's how it works:

- Define key variables: Interest rates, revenue growth, default correlations, recovery rates

- Run random samplings: Simulate thousands of scenarios (often 10,000+) with different combinations of these variables

- Observe outcomes: Analyze the distribution of portfolio losses, defaults, and rating migrations across all scenarios

- Assess risk: Estimate probabilities of losses exceeding certain thresholds and understand tail risks

Monte Carlo simulations excel at stress-testing portfolios and understanding correlated default risk during recessions, which simpler models often overlook. However, outputs are only as reliable as the input assumptions and correlations that are modeled, making careful calibration essential.

Advanced AI and Machine Learning

Advanced AI in credit risk now looks less like a single model and more like a coordinated system for analyzing the structured and unstructured data that traditional models often miss.

While statistical models still play a core role in estimating PD, LGD, and EAD, AI financial modeling adds another layer by helping teams interpret the legal, operational, and market context that shapes real credit outcomes.

This matters because modern credit workflows extend far beyond spreadsheets. Teams need to review credit agreements, amendments, compliance certificates, SEC filings, earnings transcripts, portfolio reporting, and virtual data room (VDR) materials—often under tight deadlines and across large portfolios.

Tools like Hebbia leverage natural language processing (NLP) and advanced architectures, such as Iterative Source Decomposition (ISD), to parse and understand context, sentiment, and nuanced language in documentation in a fraction of the time it would take to do so manually.

AI is especially valuable in workflows like:

- Covenant tracking: AI automatically extracts and monitors complex benchmarks, timelines, and restrictions across hundreds of credit agreements, surfacing compliance risks before they become breaches.

- Signal detection: AI identifies weak signals or loopholes in dense documentation that could allow borrowers to shift collateral, take on additional debt, or otherwise diminish lender protections—risks that manual review would miss.

- Enhanced diligence: AI synthesizes disparate data sources—credit agreements, SEC filings, earnings transcripts, proprietary investment committee (IC memos—into risk-focused investment memos with perfect accuracy and in-line citations.

- Portfolio monitoring: AI processes real-time market data, news, and rating actions to flag early warning signs of credit deterioration across hundreds of positions simultaneously.

AI surfaces forward-looking risks hidden in contract language, management commentary, and market signals. With 34% of financial professionals struggling to analyze mixed qualitative and quantitative data, AI helps bridge the gap between structured metrics and the unstructured information that often reveals risk first.

Uncover hidden risks before they impact returns.

Hebbia's AI platform processes credit agreements, financial filings, and portfolio data at scale—surfacing covenant risks, performance deterioration, and early warning signals that traditional models miss so that you can protect downside with precision and speed.

Common Challenges in Credit Risk Modeling

Even well-designed models break when the operating environment changes or the data pipeline is incomplete. The most common failure points today are:

- Fragmented data sources: Credit teams rarely work from a single source of truth. When key risk signals are scattered across systems and document types, it becomes harder to build a complete view of borrower health and easier for important details to be missed.

- Documentation oversight: Many models still focus heavily on financial metrics while giving less weight to the legal terms that shape real downside protection. In practice, permissive covenant language or structural loopholes can materially change risk even when headline leverage appears unchanged.

- Model drift: Credit models are only as useful as the assumptions behind them. When market conditions or borrower performance shift quickly, models calibrated to prior environments can become less reliable and fail to reflect current risk.

- Weak explainability: More advanced models can improve pattern recognition, but they also introduce oversight challenges. If teams cannot clearly explain how outputs were generated or validate them against documented standards, adoption becomes harder in high-stakes credit workflows.

- Deployment constraints: Even when AI or modeling tools are effective, firms may hesitate to scale them if they cannot meet internal security, privacy, and access-control requirements. In credit, where workflows often depend on sensitive borrower materials and internal research, weak governance can become a barrier to broader use.

These are operational problems as much as modeling problems. Fixing them requires better data lineage, clearer validation standards, and infrastructure that can handle private documents securely at institutional scale.

Global Regulations and Regulatory Frameworks (2026 Outlook)

The regulatory landscape for 2026 reflects a global push toward forward-looking risk assessment and total transparency. While these standards are mandatory for banks, they increasingly define the best practices that private credit funds must follow to remain competitive and compliant in a tightening market.

- Basel III & Basel IV: These frameworks establish the finalized global standards for capital adequacy and financial risk management. For private credit, the output floor in Basel IV influences how the banks providing your leverage facilities calculate risk, directly impacting the cost and availability of fund-level financing.

- IFRS 9 and CECL: These standards shift the focus from incurred losses to expected credit losses (ECL). For private credit investors, this requires more sophisticated modeling that can predict potential losses over the entire life of a loan using both historical data and forward-looking macro assumptions.

- ESG integration: In some markets, embedding environmental, social, and governance (ESG) risks into credit assessment is no longer optional. Under guidelines such as those from the European Banking Authority, credit analysts must now treat ESG factors as material financial risks that can affect a borrower's long-term default probability.

- Stress testing: Regulatory bodies now mandate simulations to assess portfolio resilience under "extreme but plausible" adverse conditions. Private credit funds increasingly use these simulations to justify their risk appetite to investors and ensure they can withstand significant market shocks without breaching their own leverage covenants.

How Hebbia Accelerates Accuracy in Credit Risk Modeling

Credit risk modeling depends on accurate inputs, including financial metrics and recovery assumptions. Traditional financial modeling software relies on manual extraction, a process that's time-consuming, error-prone, and struggles to surface the nuanced language that defines real risk.

Hebbia unifies fragmented data—from credit agreements to VDRs—into one traceable workflow. It analyzes text and visuals across massive datasets with built-in citations for easy verification.

For credit teams, that means faster covenant reviews, tighter monitoring, more defensible IC materials, and earlier visibility into risks that spreadsheet-only processes tend to miss.

If your process still depends on manual extraction before anyone can analyze the real downside, book a demo with Hebbia to move faster on the risks that matter most.