AI in Credit Risk Management: Evolution, Impact, and Essentials

Credit teams face an impossible tradeoff: The volume of data required to properly assess risk has exploded, yet the time available to analyze it hasn't changed. Every loan agreement contains hundreds of pages of covenants, financial metrics, and legal provisions—any one of which could signal future distress. Miss a critical term buried in a credit agreement, and the downside could be catastrophic.

Traditional risk models and manual document review simply can't keep pace with modern credit portfolios. Enter Generative AI, which is fundamentally changing how credit teams approach risk assessment.

This article examines the limitations of legacy credit scoring models, explores high-impact use cases where AI automates complex financial analysis, and outlines how leading credit organizations are using AI to uncover hidden risks faster and with greater accuracy than ever before.

What Is AI in Credit Risk Management?

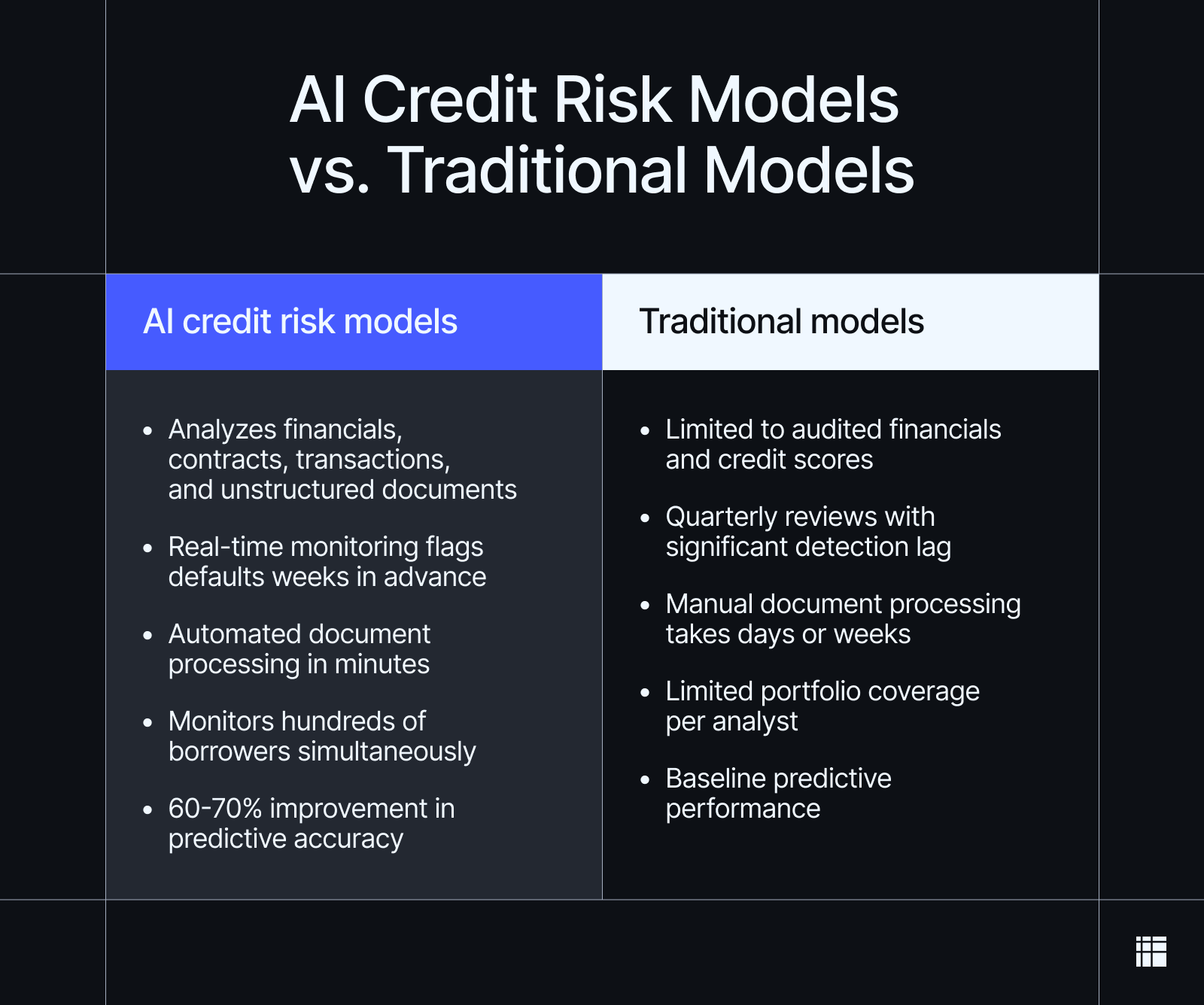

AI in credit risk management uses machine learning to identify, measure, and mitigate the risk of borrower default in commercial lending. Unlike traditional credit models that rely on limited financial ratios and historical performance data, AI-driven financial risk management software analyzes thousands of data points across financial statements, credit agreements, market data, and unstructured documents to assess creditworthiness and ongoing risk.

The industry standard has evolved beyond single-model approaches to composite AI frameworks, where specialized models handle distinct aspects of the credit lifecycle. One agent might extract covenant terms from loan documentation, while another monitors financial performance against benchmarks, and a third flags early warning signals from market data.

Hebbia's Matrix platform puts this into practice. When assessing a borrower's compliance across multiple loan agreements, Matrix breaks down the analysis into specialized tasks—extracting covenants, monitoring financial metrics, and identifying risks—and runs them simultaneously through dedicated AI agents, delivering comprehensive assessments in minutes rather than days.

How Credit Professionals Use AI to Manage Risk

Credit professionals use AI across the entire lending lifecycle, from initial underwriting to ongoing portfolio management. The highest-impact applications focus on parsing dense legal documentation, automating covenant compliance tracking, and surfacing early warning signals that manual review would miss.

Below are the core use cases where AI delivers measurable improvements in speed, accuracy, and risk mitigation.

Use case | What AI does | Key benefit |

|---|---|---|

Enhanced credit scoring | Analyzes non-traditional data sources and identifies creditworthy borrowers that traditional models miss | Expands investable universe without increasing risk |

Default prediction | Monitors real-time behavioral signals (transaction volumes, payment patterns, cash management) | Flags potential defaults weeks before traditional metrics detect them |

Automated credit memos | Processes entire data rooms and extracts financial metrics, covenants, and risks with inline citations | Reduces memo creation from weeks to days while maintaining accuracy |

Enhanced Credit Scoring and Underwriting

AI credit scoring and underwriting expand the investable universe by identifying creditworthy borrowers that traditional models miss. For example, AI can:

- Analyze non-traditional data sources: AI parses management documents, supplier contracts, customer concentration data, and cash flow patterns that go beyond audited financials.

- Assess operational resilience: The technology evaluates recurring revenue stability, customer retention metrics, and business model durability across unstructured documents.

- Surface "invisible prime" borrowers: AI identifies creditworthy private companies that traditional models reject due to complex ownership structures or non-standard financial reporting.

Traditional credit models often miss these opportunities because they rely on standardized financial structures and conventional data markers. For private credit funds evaluating a leveraged buyout, generative AI can build comprehensive risk profiles from hundreds of documents, expanding the fund's opportunity set without increasing risk.

Default and Loss Prediction

Early warning signals often appear in operational behavior long before they show up in financial statements or credit bureau reports. Traditional credit monitoring relies on quarterly financials and monthly bureau updates, creating a lag that can cost lenders millions in preventable losses.

AI detects behavioral signals that predict defaults weeks in advance, such as:

- Transaction volume changes: AI flags measurable declines in B2B transaction volume or sales velocity, such as a 10% month-over-month drop, that indicate weakening demand or operational stress.

- Payment prioritization shifts: The system detects delayed payments to non-critical suppliers while borrowers continue paying key vendors, signaling cash constraints.

- Cash management patterns: AI identifies changes in cash conversion cycles or liquidity management behaviors that suggest operational stress.

- Operational anomalies: The technology surfaces unusual banking activity or deviations from historical spending patterns that may indicate financial distress.

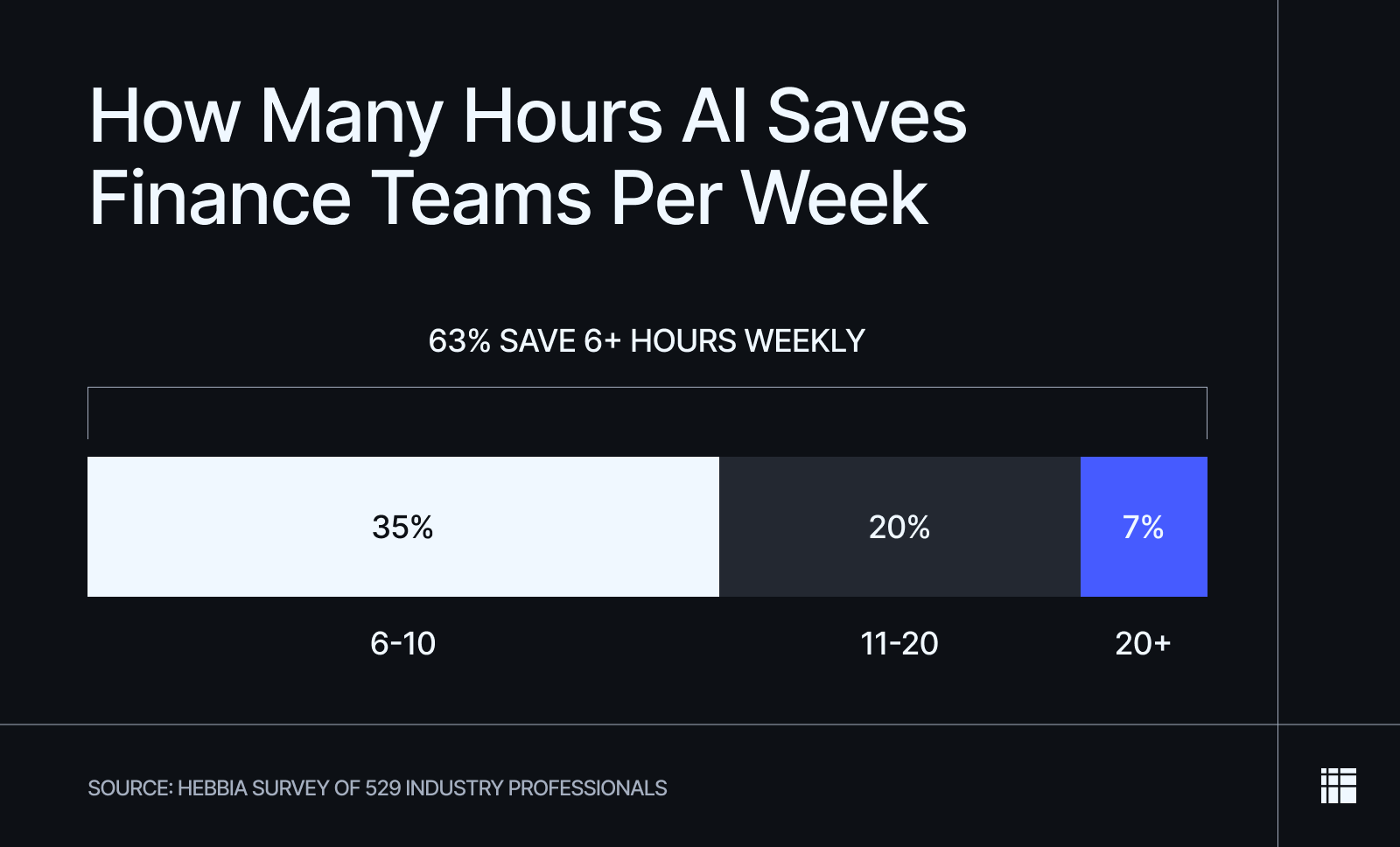

For credit portfolios monitoring dozens (or hundreds) of borrowers simultaneously, AI continuously processes transaction data, banking activity, and market signals in real time. In a recent survey, 63% of finance professionals reported saving at least six hours per week by using AI for research and analysis, with credit and portfolio monitoring among the top use cases.

This predictive edge allows credit teams to take proactive measures (adjusting covenant terms, increasing monitoring frequency, or initiating early workouts) before defaults materialize and losses compound.

Automated Credit Memos and Documentation

Credit memos are the foundation of investment committee decisions, and their quality directly impacts deal approval and portfolio performance. Building a comprehensive memo traditionally requires analysts to spend days or weeks on:

- Document synthesis: Reviewing thousands of pages across CIMs, tax returns, industry reports, management presentations, and historical financials

- Data extraction: Pulling financial metrics, covenant terms, and risk factors from unstructured documents

- Cross-referencing: Validating assumptions and identifying inconsistencies across multiple data sources

- Citation tracking: Manually documenting the source of every claim and assumption

AI automates synthesis and documentation while preserving the analyst's judgment in assessing credit quality. Platforms like Hebbia's Matrix process entire virtual data rooms (VDRs) simultaneously, extracting relevant financial metrics, covenant terms, and risk factors across hundreds of documents, then organizing them into a structured memo format with inline citations.

Benefits of AI Credit Risk Technology

AI credit risk tools deliver measurable improvements across prediction accuracy, capital efficiency, and operational speed. These advantages compound over time: Better risk assessment leads to stronger portfolio performance, while faster processing allows credit teams to evaluate more opportunities without adding headcount.

The result is a fundamental shift in how credit organizations allocate resources and capital:

- Sharper predictive power: AI-driven credit risk technology can achieve a Gini coefficient (a measure of model accuracy) that’s 60 to 70% higher compared to traditional credit risk models. In practice, this means fewer yield traps—avoiding borrowers that appear creditworthy but carry hidden risks—and better identification of high-quality private companies that traditional filters would reject due to non-standard financial structures.

- Capital efficiency (RWA optimization): High-fidelity AI models provide regulators with more granular, defensible risk data, which can justify lower risk-weighted asset (RWA) calculations and reduced capital reserve requirements. This unlocks capital that was previously held in reserve, allowing firms to deploy more capital into new deals without raising additional funds.

- Operational velocity and STP: AI extracts initial data from confidential information memos (CIMs), financial statements, and supporting documents, reducing deal triage from hours to seconds. This straight-through processing (STP) allows credit teams to focus on complex deal structuring, covenant negotiation, and risk assessment rather than manual data entry and document review.

Challenges and Compliance Implications

While AI delivers measurable improvements in credit risk assessment, implementation comes with regulatory and operational risks that credit institutions must manage carefully:

- Explainability: Regulators require clear, defensible reason codes for credit denials and adverse actions. Global mandates like the EU AI Act demand transparency in how AI models reach decisions, making black-box approaches unusable in regulated lending environments. Credit institutions must be able to explain every decision to borrowers, regulators, and internal audit teams with specific, traceable logic.

- Model drift: Credit models trained on historical data can become obsolete during sudden economic shifts, a phenomenon known as model drift. When macroeconomic conditions change rapidly (interest rate shocks, recession, sector-specific stress), models that performed well in stable periods may fail to accurately predict risk. This requires continuous model monitoring, stress testing across different economic scenarios, and rapid recalibration capabilities.

- Algorithmic bias: AI models trained on historical lending data can reproduce past discriminatory patterns, even when protected characteristics like race or gender aren't explicitly used as inputs. Seemingly neutral variables (such as zip code, education level, or employment type) can serve as proxies for protected classes, leading to indirect discrimination. Regulators monitor for redlining and disparate impact, requiring institutions to validate that their models produce fair outcomes across all demographic groups through rigorous bias testing and ongoing monitoring.

- Third-party and concentration risk: Many institutions rely on a small pool of specialized AI vendors, creating concentration risk across the industry. Regulators now emphasize model risk management (MRM) frameworks for third-party models, requiring institutions to conduct deep-dive audits of vendor data sources, model assumptions, and validation processes. Even when licensing a model from a vendor, the lending institution remains 100% liable for its decisions, making thorough due diligence and ongoing oversight non-negotiable.

Best Practices for Implementing AI Credit Risk Management Tools

Successful AI implementation in credit risk management requires careful planning, rigorous testing, and ongoing oversight to balance automation with human judgment while maintaining data quality and model performance.

To maximize success and minimize risk when implementing AI credit tools, prioritize these four practices:

- Execute a 6-month shadow mode trial: Run the AI model in parallel with your existing system for at least two quarters without allowing it to influence lending decisions. This allows you to compare the AI's predictions against actual default outcomes, identify false positives before putting capital at risk, and build institutional confidence in the model's reliability.

- Standardize Human-in-the-Loop (HITL) thresholds: Establish clear escalation rules so that AI handles routine assessments, while senior credit officers make final decisions on complex or high-value loans. For deals above certain thresholds or with unusual structures, AI should extract data and flag risks while experienced underwriters provide final judgment on edge cases the model hasn't encountered.

- Transition to a unified credit data lake: Eliminate silos between unstructured document repositories (VDRs, CIMs, financial statements) and structured core banking systems by implementing a centralized platform where all credit-relevant information is accessible. This ensures AI models have complete, high-quality data across both structured and unstructured sources, preventing misinformed decisions based on partial information.

- Implement AgentOps for model monitoring: Deploy real-time dashboards that track model drift, prediction accuracy, and algorithmic bias, with automated triggers that alert risk teams when performance drops below acceptable thresholds. Static annual audits are insufficient in dynamic credit markets—continuous monitoring allows you to detect and address performance degradation before it impacts lending decisions or regulatory compliance.

Using Hebbia for Credit Risk Management

Modern AI in credit risk management has evolved from a simple scoring tool into a comprehensive operational engine. By combining alternative data, real-time surveillance, and a composite AI architecture, financial institutions can now achieve higher predictive accuracy while meeting strict regulatory standards for explainability.

Hebbia's Matrix platform streamlines this evolution by using agentic orchestration to automate the synthesis of thousands of unstructured documents, from credit agreements to complex tax returns. This allows your team to generate cited, professional credit memos in minutes and benchmark risks against your entire institutional memory.

Ready to see how Hebbia can transform your credit workflow? Request a demo with Hebbia today.